Over 70 percent of global banking customers now prefer mobile apps over physical branches. In India alone, UPI transactions crossed billions per month. Digital-first banks like Revolut and N26 acquired millions of users without owning a single branch.

This is no longer a trend. It is infrastructure. If your institution is still treating mobile banking as a secondary channel, you are already competing at a disadvantage. But here is the real challenge. Most banks struggle not with the idea of building a mobile banking app. They struggle with building it right.

Security concerns. Regulatory pressure. Legacy system integration. Cost uncertainty. Vendor selection confusion.

Do you want to learn all about this? Let us simplify this. This guide will help you understand.

What Is Mobile Banking Application Development?

Mobile application development is not simply about building an app that shows balances and enables transfers. It is about creating a secure digital financial ecosystem that becomes the primary interaction channel between a bank and its customers.

At its core, it involves designing, engineering, integrating and maintaining a mobile platform that allows users to manage financial activities from anywhere, at any time. But for decision-makers, the definition needs to go deeper than basic functionality.

A modern mobile banking platform typically includes:

- Secure authentication systems

- Real-time transaction processing

- Core banking integration

- Compliance-driven architecture

- Data protection frameworks

- Cloud infrastructure strategy

- Ongoing monitoring and updates

Unlike traditional mobile applications, banking platforms operate in a zero-error environment. A minor glitch in a shopping app may frustrate users. A glitch in a banking application can instantly erode customer trust and raise regulatory concerns.

This is why mobile banking application development must be approached as infrastructure modernization rather than simple feature expansion.

What Are the Different Types of Mobile Application Models?

When organizations plan a mobile application strategy, the conversation often starts with features. But experienced technology leaders know that the real decision lies in choosing the right development model.

In the context of mobile banking application development, selecting the right model is even more critical. Financial platforms handle sensitive customer data, real-time transactions and strict regulatory requirements. The underlying development approach therefore plays a major role in performance, scalability and long-term maintainability.

Broadly speaking, most mobile applications are built using three primary models.

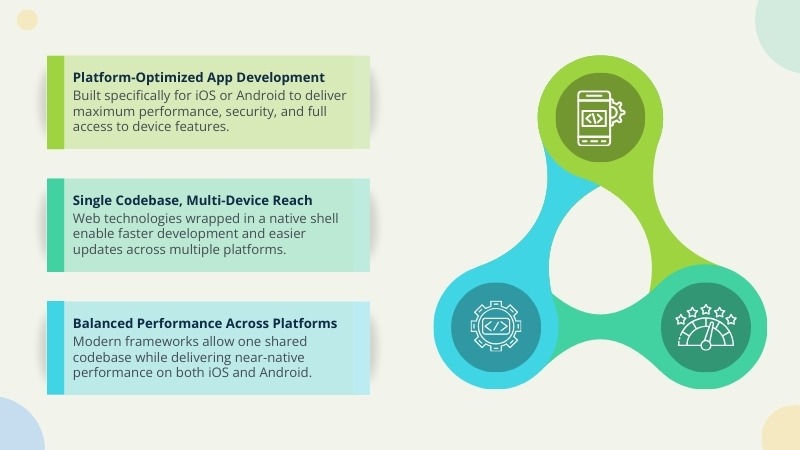

1. Native Applications:

Native apps are developed specifically for a particular operating system, such as iOS or Android. This means developers use platform-specific programming languages and tools, like Swift for iOS or Kotlin for Android.

Because these apps are designed for a single ecosystem, they deliver high performance, strong security and seamless user experiences. Native development also allows deeper access to device features such as biometrics, push notifications and secure hardware modules. The capabilities that are particularly valuable in banking applications.

The trade-off is that organizations must maintain separate codebases for different platforms, which can increase development time and cost.

2. Hybrid Applications:

Hybrid applications combine elements of web and native development. A single codebase is created using web technologies such as HTML, CSS and JavaScript and then wrapped inside a native container so it can run on multiple platforms.

This approach allows businesses to launch applications faster and manage updates more efficiently across devices. However, hybrid apps may sometimes face limitations in performance or deep hardware integration compared to fully native solutions.

For institutions looking to balance speed of deployment with cross-platform reach, hybrid development can be a practical option.

3. Cross-Platform Applications:

Cross-platform development frameworks such as Flutter or React Native allow developers to build applications that run on both iOS and Android using a shared codebase. Unlike traditional hybrid apps, these frameworks are designed to provide performance closer to native experiences.

For many organizations, this model offers a balance between efficiency and performance. It enables faster development cycles while still supporting rich user interfaces and essential mobile features.

Why Do So Many Mobile Banking Projects Struggle or Fail?

If mobile banking is such a clear necessity, why do so many institutions delay it, over-budget it, or quietly scale back their ambitions? The answer is not lack of intent. It is complex.

Let us talk honestly about what leadership teams face behind closed doors.

1. Legacy Infrastructure That Was Never Built for Mobile:

Many banks still rely on core systems that were designed decades ago. These platforms were originally built for branch operations and batch processing rather than real-time APIs and mobile-first interactions.

When a modern mobile application needs to communicate with outdated infrastructure, integration quickly becomes fragile. Development timelines stretch longer than expected, costs increase and potential security gaps begin to appear.

The result is often a mobile app that looks modern on the surface but struggles to deliver consistent performance behind the scenes.

Why Does Security Anxiety Slow Down Mobile Banking Initiatives?

Financial data is one of the most targeted assets in the world. A single breach can damage brand trust overnight and trigger serious regulatory consequences.

Leadership teams often worry about several critical areas:

- Data encryption standards

- Fraud detection capabilities

- Authentication vulnerabilities

- Risks introduced through third-party integrations

These concerns are entirely valid. However, delaying mobile banking development does not eliminate security risk. In many cases, it simply allows competitors to move ahead. The smarter approach is designing a security-first architecture from the very beginning.

Why Does Regulatory Compliance Feel So Complex?

Financial institutions operate in one of the most heavily regulated industries. Depending on geography, organizations may need to comply with frameworks such as

- PCI-DSS

- GDPR

- PSD2

- Local central bank regulations

Compliance is not just a legal requirement. It directly influences application architecture, data storage policies, authentication methods and audit capabilities. When regulatory considerations are introduced late in the development cycle, organizations often face expensive redesigns and delays.

Why Is Budget Uncertainty a Major Concern for Leadership?

One of the most common questions executives ask is straightforward: How much will this project actually cost? Without a structured roadmap, mobile banking projects can quickly expand in scope.

Feature additions, unexpected integrations and redesign cycles often inflate the initial budget. This uncertainty can create hesitation at the board level. A clearly defined scope combined with a phased rollout strategy helps organizations maintain financial control while still delivering meaningful innovation.

What If Customers Don’t Adopt the App?

Another concern that many institutions hesitate to voice openly is adoption. Building a mobile platform is one challenge; getting customers to actively use it is another.

If onboarding feels complicated or the app performance is inconsistent, user engagement drops quickly. When that happens, organizations often increase marketing spend just to drive adoption.

Customer expectations today are shaped by companies like Amazon, Apple and Google. Banking applications are no longer compared only to other banks. They are compared to the best digital experiences people encounter every day.

How Can Financial Institutions Build a Secure and Scalable Mobile Banking Platform?

The difference between a struggling mobile banking initiative and a successful one is not budget size. It is planning depth. When approached strategically, mobile banking development becomes predictable, measurable and aligned with business growth goals.

Let us walk through what that looks like.

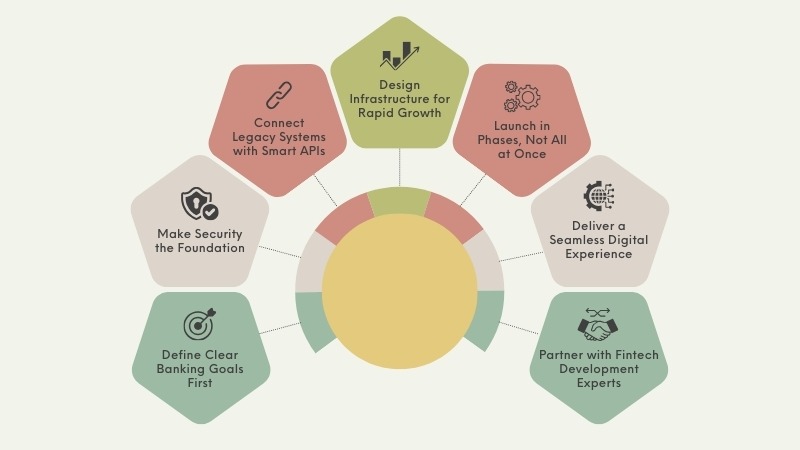

1. Start With Business Objectives:

Many institutions begin by listing features. That is backwards. Instead, leadership should first define:

- Are we trying to increase customer acquisition?

- Reduce branch operational costs?

- Improve cross-selling of loans and investments?

- Expand into new geographic markets?

When business goals are clear, feature prioritization becomes easier and waste reduces dramatically. For example, if your objective is improving customer retention, AI-powered financial insights and personalized alerts may deliver a stronger impact than launching investment modules immediately.

Clarity at this stage prevents expensive rework later.

2. Design Around Security:

Security cannot be layered after development. It must shape architecture. A future-ready mobile banking platform includes:

- End-to-end encryption

- Multi-factor authentication

- Device binding

- Behavior-based fraud detection

- Secure API gateways

- Continuous penetration testing

Cloud-native environments configured correctly are highly secure. What matters is governance, monitoring, and identity management. Institutions that integrate DevSecOps practices during development experience fewer post-launch vulnerabilities.

Teams with mature cloud and DevOps expertise, such as those specializing in secure infrastructure engineering like SoftProdigy, help embed this discipline early in the lifecycle. Security-first architecture builds confidence across leadership, regulators, and customers.

3. Modernize Integration With API Architecture:

Legacy systems do not need to be replaced overnight. Instead, many successful banks adopt an API gateway and middleware approach. This creates a secure bridge between traditional core systems and modern mobile interfaces.

Microservices architecture improves flexibility. Each service can scale independently. Updates can be deployed without disrupting the entire system. This approach reduces long-term technical debt and prepares the institution for open banking ecosystems.

Related Read: AI-Driven Legacy App Modernization: Cut Migration Time and Costs by 70%

4. Build for Scalability:

User growth can spike unexpectedly. Campaign success, partnerships or regulatory changes can drive rapid adoption. If infrastructure is not elastic, downtime becomes a risk. Cloud-based deployments with auto-scaling and real-time monitoring provide resilience. Uptime is not just technical reliability. It is brand credibility.

When customers cannot access their funds, trust erodes quickly.

5. Adopt a Phased Development Strategy

A phased rollout minimizes risk.

- Phase one can include core features such as account management, transfers, and secure login.

- Phase two may introduce advanced modules such as lending, investments, and AI-based analytics.

This approach allows leadership to measure adoption, gather feedback, and refine product strategy before scaling further. It also spreads investment over predictable milestones.

6. Invest in User Experience:

Customers rarely praise security explicitly, but they immediately notice friction. Digital experiences must feel effortless even when complex systems operate underneath.

7. Choose Technology Partners With Financial Domain Expertise:

Software engineers who combine product engineering and mobile banking application development are not generic software engineers. Financial compliance, risk frameworks, and data sensitivity require specialized experience.

Before committing to a vendor, evaluate:

- experience with regulated industries

- approach to secure coding practices

- ability to handle long-term maintenance

- cloud and AI capabilities

Essential Features of Modern Mobile Banking Applications

Successful banking applications combine security, convenience and financial insight.

Key features typically include

- Account balance and transaction history

- Secure fund transfers

- Bill payments and scheduled transactions

- Push notifications for account activity

- Biometric authentication

- Card management and transaction controls

Advanced capabilities are also becoming common. AI-driven spending insights help customers understand financial behavior. Fraud detection systems analyze unusual activity in real time. Digital onboarding enables customers to open accounts without visiting a branch.

Banks that integrate these capabilities improve user engagement and retention.

How Much Does Mobile Banking Application Development Cost?

Development costs vary depending on complexity and compliance requirements.

Typical ranges include:

- Basic MVP platforms may cost between $80,000 and $120,000.

- Mid-scale banking applications with expanded functionality often range between $150,000 and $250,000.

- Enterprise banking ecosystems that include advanced analytics, regulatory integrations and high-scale infrastructure can exceed $300,000.

While cost is an important factor, reliability, security, and scalability should remain the primary decision criteria.

Emerging Trends in Mobile Banking for 2026

Several innovations are reshaping the future of digital banking.

- Artificial intelligence enables predictive financial insights and automated fraud detection.

- Embedded finance allows banking services to integrate into non-bank platforms.

- Voice-enabled banking interactions are becoming more common.

- Open banking ecosystems enable collaboration between financial institutions and fintech platforms.

- Institutions that adopt these technologies responsibly will gain competitive advantages.

Conclusion,

Technologies like artificial intelligence, embedded finance, voice banking and open banking are reshaping how financial services are delivered. Customers now expect banking to be instant, intelligent and seamlessly integrated into their digital lives.

To meet these expectations, mobile banking platforms must evolve beyond basic transactions and become secure, scalable financial ecosystems that support continuous innovation.

At Softprodigy, we help financial institutions build mobile banking solutions that combine secure architecture, seamless user experience, and regulatory readiness.

Planning your next-generation mobile banking platform? Connect with Softprodigy’s fintech experts to explore the right development strategy for your organization.